updated Apr 17, 2024: pre-meeting prep

-

The main argument is that patents are valuable intangible asset to the firm and can help the firm reduce their cost of debt.

-

Mann (2018) has shows that mature firms use patents as collateral for future debt financing. He uses four decision dates as shock to strengthen the creditors rights to the underlying intangible collateral to show that treated firms increase their debt to asset ratio and R&D-to-asset ratio after the treatment. ^mann_2018

-

Hochberg et al. (2018) look into the lending to startups and link the redeployability of patents to its usage of collateral in the venture debt market. By the way, lenders also value the pool of their equity investor in the lending relationship.

-

Roberts and Sufi (2009) study the renegotiation process of private credits agreements between US public firms and financial institutions, with 90% long term debts being renegotiated. They conclude that the accrual of new information and changes in macro environment as the main drivers for renegotiation and the direction of the outcome is determined by the bargaining power of contractual parties.

- Does an increasing portfolio of newly granted patents incentivise the firm to renegotiation their existing private credits, especially in a relatively loose financial environment?

-

Becker et al. (2024) for callable bond and proposes that the “credit role”, different from the “interest rate view” play a crucial role in the callable bond market, in both inclusion and exercises.

- Q: What if callable bonds only present as a signal that the firm is in good quality? however, the reality that bonds are not called back means that the manager might be incompetent. Therefore, these firms, still having a large amount of callable debt outstanding, are more likely to be acquired. The subsequent investment & payout may also be the result of mismanagement.

- So, I conjecture that some time-varying top management behavior may be the unobserved confounders in this relationship. Also, investment inputs and outputs are two distinct aspects and should also be studied.

-

Roberts (2015) shows that even long-term bank loans are frequently renegotiated, even when no covenant is violated. > example of SEC filing

-

Chernenko et al. (2022) document that a large number of firms borrow from non-banks.

-

Potential exogenous shock in mind: the underlying idea is that under some exogneous, state or county level shocks,

- the intensification of local competition in the lending market -> ? ;

- the introduction of new airline, railroad, high speed railway -> faciliate the information transimission and cost of renegotiation;

Are firms with more unpledged patents more likely to renegotiate their existing debt contract and obtain more favorable terms.

Or are they more likely to get less severe punishment in the case of covenent violation? -

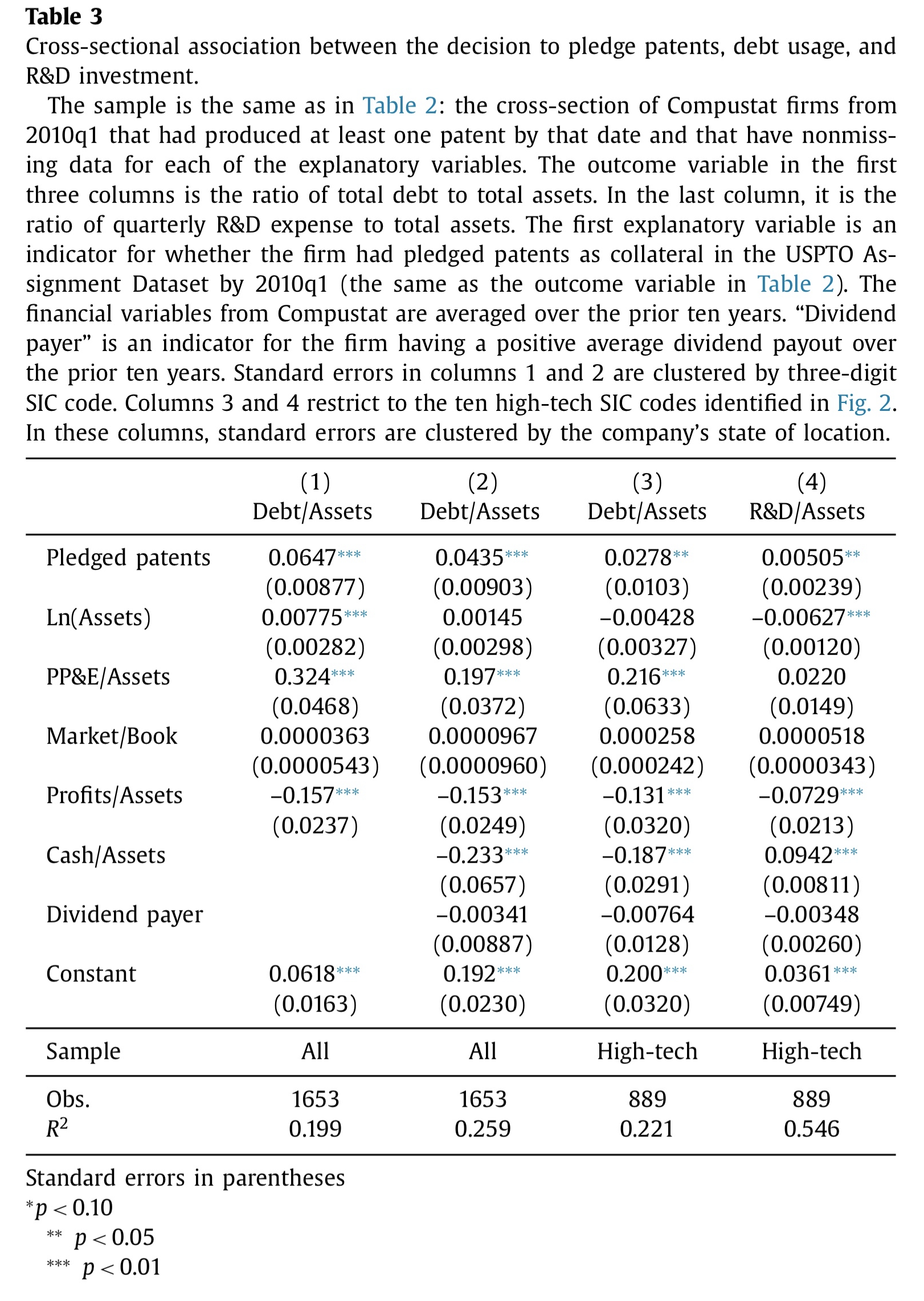

Some preliminary results: OLS with FEs ; supporting Mann (2018) Table 3

{kind=link}

updated Apr 18, 2024: advice from Bo and following brain-storm

-

The better research question: what are the determinants of borrower initiated renegotiations?

- Q: Renegotiation with good news.

- Q: How does renegotiations /the option to renegotiated benefits the borrower?

- Motivation: bad news has been studied extensively and (potential) covenants violation has been an important determinant for creditor initiated renegotiations. However, they are no studies on the positive benefits of loan/credit renegotiations, relative to bonds which cannot be renegotiated.

- The ranking of debts with different level of flexibility: Loans/credit lines/Private credits > Sydicated loans > callable bonds > bonds.

- Sydicated loans can be repaid in advance and issue a new one, although with a cost.

- Prepayment is allowed; however, there is a cost.

- Need to remeber that there is a cost associated with issuing a new loan/debt (approx. 1% or 20bps for a five year bond).

[!IMPORTANT] Q: why does the borrower need to renegotiate their current debts?

- A: A key answer is that the previous debt contract may contain certain restrictions on the (i) firm's leverage, (ii) ability to access capital market in the future and (iii) capital expanditure/investments. An increase in either the value of current patent portfolio or the amount of pledgable patents in the firm’s patent portfolio should be seen as a positive signal and encourgaes the creditor to take more risk in this lending relationship.

updated Apr 23, 2024: cts lit review

- Ma et al. (2024) find that lenders imporse stricter covenants for firms filing more patents. This relationship is stronger when the creditor has expertise and the borrower has a higher default risk. They argue that since these firms face greater future product commercialisation and operating uncertainties, more discipline is required by the creditor when designing the contract.

- This evidence combined with Mann (2018) shows that the additional loans granted after creditor control rights enhancement also faces restrictions imposed by existing creditors. The loan renegotiation will be a much more convincing mechanism that leads to this result.

- Also relate to the KPSS (2017), the value created by the loan renegotiation can spillover to the equity market. (debt $\rightarrow$ equity) and this is supported by Godlewski (2015).

[!IMPORTANT] Check this paper: Addoum, J.M., Murfin, J.R., 2020. Equity Price Discovery with Informed Private Debt. The Review of Financial Studies 33, 3766–3803. https://doi.org/10.1093/rfs/hhz128.

- Comments from Alexander: Apr 23, 2024

- Why does the firm not use patents as collaterl to get new debts?

- Still seems to be a bit too small.

- Need to see what is the question in the debt renegotiation literature.

- Updated Apr 20, 2024